| Bottom Line

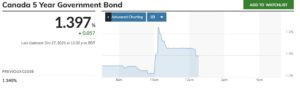

Since the Bank last met in early September, the Government of Canada five-year bond yield has spiked from .80% by a whopping 60 basis points to a 1.40%. That is an incredible 75% rise. A year ago, the five-year bond yield was only .37%.

The Bank believes the surge in inflation is transitory, but that does not mean it will be brief. CPI inflation was 4.4% y/y in September and is expected to rise and average around 4.75% over the remainder of this year. Macklem now believes inflation will remain above the Bank’s 1%-to-3% target band until late next year.

There is also a good deal of uncertainty about the size of the slack in the economy. This is always hard to measure, especially now when unemployment remains elevated at 6.9%, while sectors such as restaurants and retail are fraught with labour shortages. Structural changes in the labour force are afoot. Many former restaurant employees have moved on or are reluctant to return to jobs where virus contagion risks and poor working conditions. There was also a surge in early retirements during the pandemic and a dearth of new immigrants.

Concerning housing, the MPR says the following: “Housing market activity is anticipated to remain elevated over 2022 and 2023 after having moderated from recent record-high levels. Increased immigration, solid income levels and favourable financing conditions will support ongoing strength. New construction will add to the supply of houses and should help soften house price growth.” |