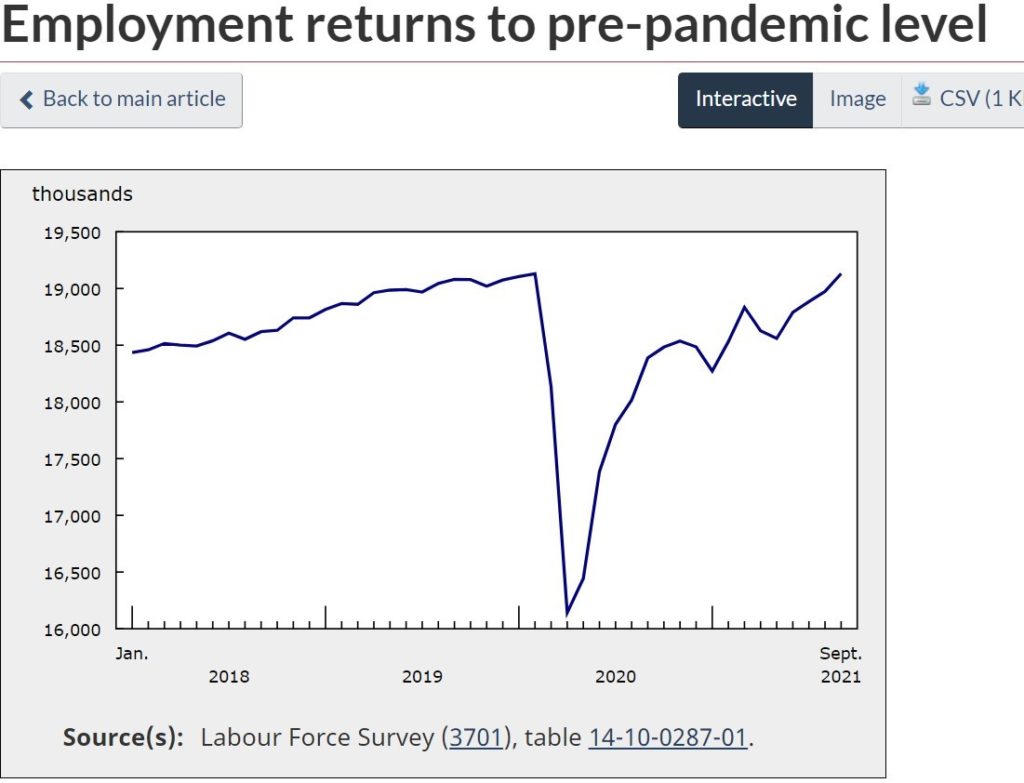

| Statistics Canada released the September Labour Force Survey this morning, providing some unmitigated good news on the jobs front. Employment rose by 157,000 (+0.8%) in September, the fourth consecutive monthly increase. The unemployment rate fell by 0.2 percentage points to 6.9%.

Employment gains in September were concentrated in full-time work and among people in the core working-age group of 25 to 54. Increases were spread across multiple industries and provinces.

Employment gains in the month were split between the public-sector (+78,000; +1.9%) and the private-sector (+98,000; +0.8%).

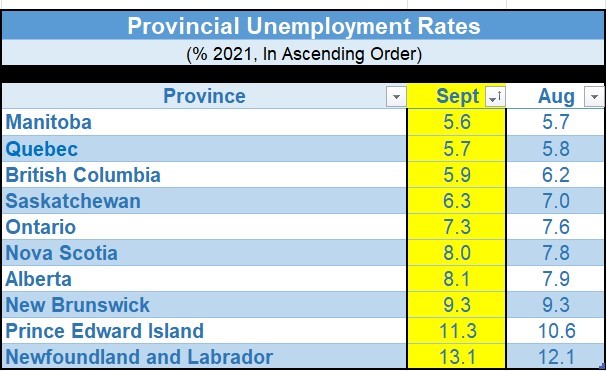

Employment increased in six provinces in September: Ontario, Quebec, Alberta, Manitoba, New Brunswick and Saskatchewan.

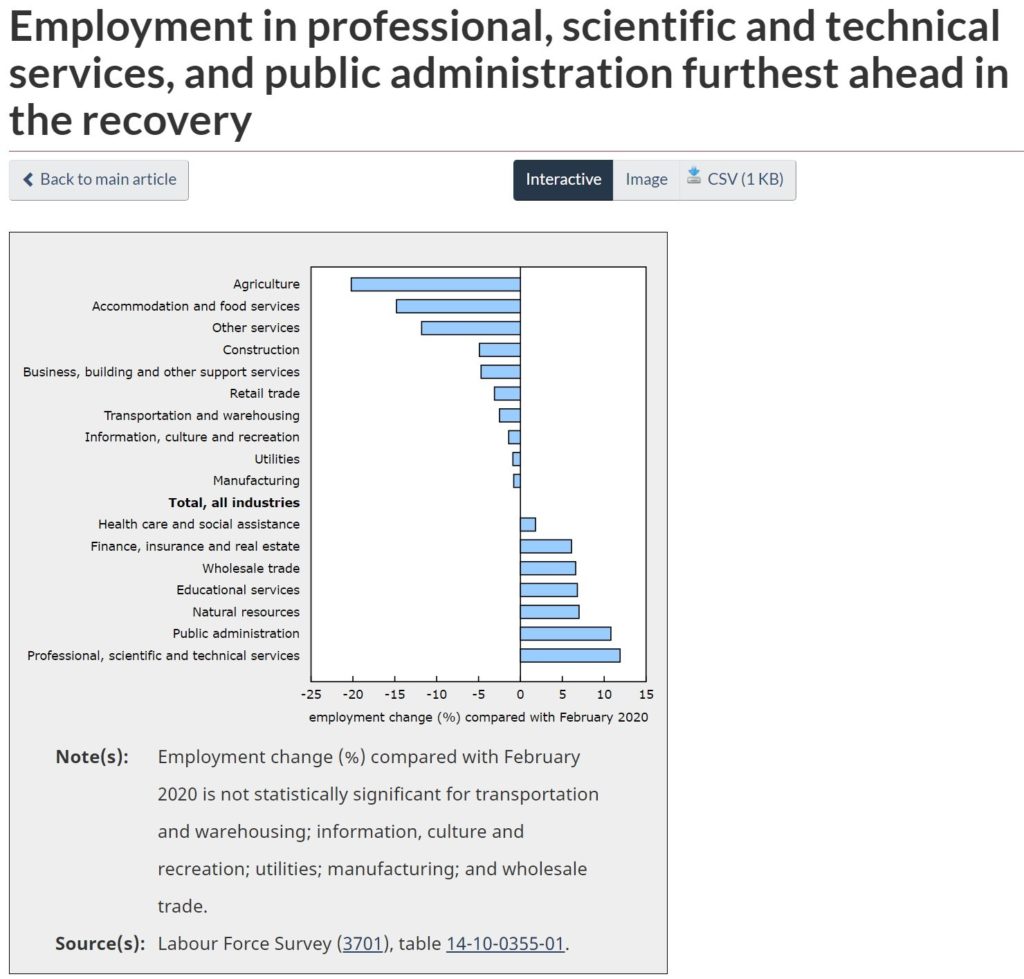

Service-sector increases (+142,000) were led by public administration (+37,000), information, culture and recreation (+33,000) and professional, scientific and technical services (+30,000).

Employment in accommodation and food services fell for the first time in five months (-27,000).

While employment in manufacturing (+22,000) and natural resources (+6,600) increased, there was little overall change in the goods-producing sector.

The gains in September brought employment back to the same level as in February 2020, just before the onset of the pandemic. However, the employment rate—that is, the proportion of the population aged 15 and older employed—was 60.9% in September, 0.9 percentage points lower than in February 2020, due to population growth of 1.4% over the past 19 months.

The number of employed people working less than half their usual hours was little changed in September and remained 218,000 higher (+26.8%) than in February 2020. Total hours worked were up 1.1% in September but were 1.5% below their pre-pandemic level.

Among 15-to-69-year-olds who worked at least half their usual hours, the proportion working from home was little changed in September at 23.8%. The ratio who worked from home was lowest in Saskatchewan (12.3%) and Newfoundland and Labrador (12.8%), and highest in Ontario (28.7%). Overall, at the national level, the proportion of workers who worked from home was higher in urban areas (25.2%) than in rural areas (15.9%).

In September 2021, 4.1 million Canadians who worked at least half their usual hours worked from home, similar to the level recorded in September 2020. |